Surety Bonds vs. Insurance: What’s the Difference?

You’ve probably come across “insurance” and “surety bonds” in discussions about managing business risks, particularly in relation to contracts, construction projects, or government contracts. They sometimes seem interchangeable. However, while both are designed to safeguard your finances and mitigate risk, they’re fundamentally distinct. Their applications are varied, and they operate on entirely different principles.

For contractors, business owners, and those involved in project work, understanding the distinction between surety bonds and insurance is crucial.

What are surety bonds?

Surety bond is a contractual agreement. In this arrangement, one party, known as the principal, agrees to fulfil a particular obligation to another party, the obligee. A third party, the surety, provides a guarantee. If the principal fails to meet their commitments, perhaps by not finishing their job, the surety steps in to cover the obligee’s losses.

What distinguishes surety bonds from other types of bonds is the presence of three separate entities:

Principal: This is the company or contractor that needs to obtain the bond.

Obligee: The individual or entity demanding the bond, often a project owner or a governmental body.

Surety: The entity that guarantees the completion of the work.

Surety bonds are frequently used in bidding processes, government contracts, licensing stipulations, and large-scale projects to ensure contractual obligations are met.

What is insurance?

Insurance functions as a financial instrument, offering protection to the policyholder from financial detriment stemming from particular occurrences, such as property damage, accidents, or legal liabilities. This arrangement constitutes a contractual agreement between two entities: the insured, representing the individual or entity safeguarded by the policy, and the insurer, the organisation delivering the coverage.

When a covered event occurs, the insurer must pay the agreed sum as compensation that stated in the policy. A key aspect of this agreement is that the insured usually doesn’t have to pay the insurer back for the claim. Therefore, insurance acts as a way to protect against unexpected financial difficulties.

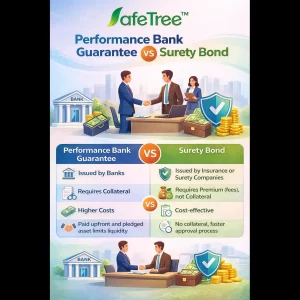

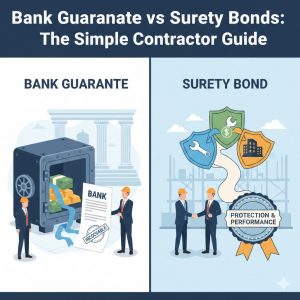

Key Differences Between Surety Bonds and Insurance

Both involve financial protection and risk evaluation, but they differ significantly in purpose, responsibility, and outcome.

1. Purpose of Protection

Surety bonds make sure that legal or contractual commitments will be met. They make sure that a project is finished or that rules are followed, and they protect the obligee, who could be a project owner or a government body.

Insurance, on the other hand, protects the policyholder against losing money because of covered risks. It protects against things like property damage, injuries, liabilities, and unexpected events, and it’s made to cover losses that aren’t certain.

2. Number of Parties Involved

A surety bond is a three-party arrangement between the principal (the person who needs the bond), the obligee (the person who is protected by the bond), and the surety (the company that guarantees the obligation).

There are two parties involved in an insurance policy: the insured (the person who buys the policy) and the insurer (the company that sells the policy).

3. Risk and Financial Responsibility

If the principal doesn’t do what they promised, the surety might pay the obligee with surety bonds. But here’s the catch: the principal has to pay the surety back for any claims that are paid. The principal is still the one who takes the risk.

If an insured loss happens, the insurance company pays according to the terms of the policy. The policyholder doesn’t have to pay the insurer back. The insurance company takes on the financial risk.

4. When Claims Are Triggered

Surety bond claims happen when the principal doesn’t follow the rules or do what they promised to do, even if there isn’t an accident or damage to property. This could mean not finishing a project, breaking license rules, or breaking a contract. Covered occurrences, like property damage, bodily injury, accidents, or liability incidents, are what cause insurance claims.

Understanding When to use a Surety Bond or Insurance

You typically need a surety bond when a government agency or project owner requires a guarantee of performance, when contractual obligations must be secured with a financial guarantee, when licensing or regulatory requirements mandate proof of financial responsibility, or when a contract demands assurance that work will be completed as agreed.

You need insurance when you want protection against unexpected or accidental losses, when you need coverage for property, equipment, employees, or liability risks, when you must protect your business from claims involving injury or damage, or when you’re legally required to carry coverage like general liability or workers’ compensation.

Conclusion

A surety bond is essentially a guarantee. It ensures that both contractual and legal obligations are fulfilled, providing a safeguard for the party expecting payment should those obligations go unmet. In contrast, insurance functions as a way to transfer risk. It safeguards the policyholder from unexpected financial losses caused by events that are covered.

Grasping this distinction is crucial for sound business decisions, regulatory adherence, and effective risk management. SafeTree helps organisations and contractors choose the right protective structure. We make the process easier, providing expert, clear, and reliable guidance.

Disclaimer:

This blog is for general informational and educational purposes only. The information related to insurance is provided for general guidance only. Before selecting any insurance policy, readers are advised to consult our insurance experts for detailed advice based on their individual needs.

Published by: A2V Insurance Brokers Pvt. Ltd. (SafeTree)

Share this post:

Facebook Twitter LinkedIn WhatsApp