Introduction

Every construction project, whether it is a sprawling residential development, a modern commercial complex, or a vital government infrastructure initiative, is a high-stakes endeavour. They demand massive financial investments, require tight coordination among dozens of stakeholders, and run on unforgiving deadlines. For project owners, the stakes couldn’t be higher. They need absolute assurance that their chosen contractors will fulfil every line of their contractual obligations. Because in this industry, even a minor delay, a sudden case of non-performance, or a contractor’s financial default can trigger catastrophic financial losses and bring work to a grinding halt. This is exactly why surety bonds have become the backbone of modern construction risk management.

At its core, a surety bond acts as a powerful financial guarantee. It ensures that contractors complete their projects according to the exact terms agreed upon, while also guaranteeing that subcontractors, suppliers, and laborers receive their hard-earned payments. By transferring a significant portion of this operational risk to a specialized surety company, these bonds foster an ecosystem of trust, accountability, and financial security. It is why they are not only a staple in public and private ventures alike, but are also rapidly outpacing traditional alternatives like bank guarantees.

From the initial bidding stage to the final handshake at project completion, surety bonds safeguard owners from default and keep the entire supply chain moving smoothly. In this article, we will explore the critical role surety bonds play in the construction industry, break down their key benefits, and look at why they have become an indispensable tool for executing successful projects in today’s competitive landscape.

What is a Surety Bond?

A surety bond is a legally binding, three-party financial guarantee used in construction to ensure a project is successfully completed. It acts as a safety net where a third-party financial institution (the surety) guarantees to the project owner (the obligee) that the contractor (the principal) will fulfil all contractual obligations, complete the work on time, and pay all subcontractors and material suppliers in full.

Why are surety bonds important in construction?

The construction sector is notoriously volatile. When massive capital investments, tight timelines, and a sprawling network of stakeholders collide, the room for error is incredibly small. If a contractor falls behind schedule, delivers subpar work, or faces a sudden financial crisis, the fallout ripples through the entire project, leading to catastrophic delays and soaring costs.

Surety bonds act as the ultimate stabilising force against these risks. Here is why they are indispensable to modern construction projects:

1. Ironclad Protection Against Contractor Default

The most critical role of a surety bond is insulating project owners from the worst-case scenario: a contractor walking away or going bankrupt mid-project. If a bonded contractor defaults, the surety company steps in to absorb the shock. Whether they compensate the owner for the financial damage or directly hire a replacement crew to finish the build, the bond ensures the project doesn’t turn into an abandoned, half-finished liability.

2. Pre-Vetted Credibility and Trust

Surety companies don’t hand out bonds to just anyone; they conduct rigorous financial, operational, and historical evaluations of a contractor before backing them. Because of this strict underwriting process, a bonded contractor carries an automatic stamp of credibility. For project owners, hiring a bonded contractor offers peace of mind that the company has the financial health and technical capability to deliver on its promises.

3. Protection for the Entire Supply Chain

A project is only as strong as its supply chain. Surety bonds (specifically payment bonds) guarantee that subcontractors, material suppliers, and labourers are paid fully and on time. By securing these payments, bonds dramatically reduce the risk of costly legal disputes, mechanics’ liens against the property, and sudden work stoppages. This keeps the workforce motivated and the supply chain moving smoothly.

4. Driving Infrastructure and Economic Growth

As public infrastructure initiatives and private developments grow larger and more complex, bank guarantees are increasingly taking a backseat to surety bonds. By unlocking liquidity and fostering accountability, bonds provide a secure framework that allows governments and private developers to fund ambitious projects with confidence, knowing public funds and private investments are safe.

Types of Surety Bonds Used in Construction

Surety bonds are not a one-size-fits-all solution; instead, they serve as specialized risk-management tools tailored to different stages of the construction lifecycle. From the initial bid submission to long after the final brick is laid, different bonds protect project owners, subcontractors, and suppliers from specific vulnerabilities.

The five most common types of surety bonds used in the construction industry include:

1. Bid Bond

Submitted during the competitive bidding process, a bid bond guarantees that the contractor is bidding in good faith. It assures the project owner that if the contractor wins the tender, they will actually sign the contract and provide the required follow-up performance and payment bonds. If the winning contractor backs out, the owner can file a claim to recover the financial difference between the low bid and the next closest bidder.

- Key Benefits: Vets out non-serious or under-qualified bidders, protects owners from sudden pricing shifts during contract awarding, and keeps the project timeline on track.

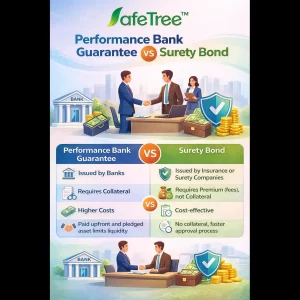

2. Performance Bond

The performance bond is the core safeguard of project execution. It guarantees that the contractor will complete the project in strict accordance with the contract’s terms, technical specifications, and deadlines. If the contractor defaults or goes bankrupt mid-construction, the surety company steps in to finish the job or financially compensate the owner.

- Key Benefits: Provides ironclad insulation against contractor default, ensures timely project completion, and maintains financial security throughout the build.

3. Payment Bond

A construction project is heavily reliant on its secondary workforce. A payment bond ensures that subcontractors, material suppliers, and labourers are paid fully and on time for their work and supplies. Because public property cannot be subjected to mechanics’ liens, payment bonds are legally mandated on public works projects (under the Miller Act in the US and similar global regulations) to protect lower-tier workers.

- Key Benefits: Minimises the risk of costly mechanics’ liens on the property, prevents labour walkouts, and fosters a reliable, motivated supply chain.

4. Maintenance Bond / Warranty Bond

Even after a project is handed over, structural or material defects can emerge. A maintenance bond (or warranty bond) protects the project owner against faults in workmanship, materials, or overall construction quality for a specified period (typically one to two years) after project completion.

- Key Benefits: Guarantees long-term quality control, covers the financial burden of post-handover repairs, and provides peace of mind after the contractor leaves the site.

5. Advance Payment Bond

It is common for project owners to provide upfront capital to help contractors mobilise equipment or secure bulk materials. An advance payment bond protects these funds, guaranteeing that the upfront cash is used strictly for the project’s designated procurement activities and protecting the owner if the contractor mismanages the funds or defaults early on.

- Key Benefits: Safely unlocks project liquidity, reduces early-stage financial risk for owners, and accelerates efficient project mobilisation.

By strategically leveraging the right combination of these bonds, project stakeholders can construct a comprehensive safety net that ensures accountability and financial stability from groundbreaking to final delivery.

Benefits of Surety Bonds in the Construction Industry

Surety bonds do far more than simply fulfil a contractual obligation; they act as a foundational pillar for successful, risk-mitigated project execution. By offering an absolute financial guarantee of both performance and payment, they foster a transparent and highly reliable environment for developers, public entities, and subcontractors alike.

Choosing a bonded framework offers several key competitive and strategic advantages:

1. Ironclad Financial Security & Risk Mitigation

The most immediate benefit is the elimination of catastrophic financial exposure. By shifting the threat of contractor default, lengthy project delays, or structural non-performance from the developer to a dedicated surety provider, project owners protect their capital investments from worst-case operational failures.

2. Immediate Boost to Contractor Credibility

A bonded contractor carries an automatic mark of distinction. Because surety providers execute rigorous financial, legal, and operational audits before backing a company, being bonded proves to the market that your business has the verified capacity, health, and history to execute high-value projects successfully.

3. Protection for the Lower-Tier Supply Chain

Payment disputes and sudden work stoppages are major threats to project timelines. Payment bonds assure subcontractors, labourers, and material suppliers that they will be paid accurately and on time. This security fosters deep trust, guarantees workforce continuity, and effectively prevents mechanics’ liens from being filed against the property.

4. Unlocked Liquidity and Better Cash Flow Management

For contractors, one of the most significant operational benefits of surety bonds over traditional bank guarantees is capital efficiency. While bank guarantees frequently freeze large lines of credit or require substantial cash collateral, surety bonds preserve a contractor’s vital working capital. This enables businesses to maintain healthy cash flow and allocate funds efficiently toward material procurement and mobilisation.

5. Increased Accountability Across All Project Phases

The presence of a three-party surety agreement naturally introduces an ecosystem of accountability. Contractors are highly incentivised to strictly adhere to contract parameters, technical specifications, and milestones, knowing that any valid claim filed against the bond requires them to fully indemnify and reimburse the surety provider.

6. Seamless Execution of Public and Mega-Infrastructure Projects

As modern public works and private commercial initiatives grow larger and more complex, managing stakeholder confidence becomes crucial. Surety bonds provide government agencies, institutional investors, and private developers with the deep baseline confidence required to confidently award and fund large-scale infrastructure developments.

Challenges Contractors Face When Obtaining Surety Bonds

While surety bonds open the door to lucrative commercial bids and public infrastructure projects, securing them is rarely a simple walk-through. Because a surety provider takes on significant financial risk by backing a business, their underwriting process is notoriously strict.

Consequently, contractors frequently run into several hurdles when trying to qualify for a bond:

1. Meeting Stringent Financial Benchmarks

The biggest barrier for most contractors is the financial vetting process. Underwriters routinely demand audited financial statements, a strong balance sheet with healthy working capital, and proof of consistent cash flow. For younger construction companies, businesses carrying heavy debt, or those navigating tight profit margins, meeting these rigid financial thresholds can be incredibly difficult.

2. Proven Track Record

Surety companies heavily favour experience. They look at a contractor’s past performance, historical project sizes, and their ability to successfully manage operational complexity. This creates a challenging paradox: to win larger contracts, you need a bond, but to get the bond, you must prove you have already executed projects of that exact scale. Emerging contractors attempting to scale up their operations often face intense scrutiny here.

3. Exhaustive Documentation and Administrative Overhead

The application process is data-heavy and time-consuming. Contractors must pull together extensive paperwork, including up-to-date Work-in-Progress (WIP) reports, bank references, detailed project histories, and resumes of key personnel. For smaller firms without a dedicated administrative team, compiling this detailed corporate data can pull valuable time away from actual job sites.

4. Overcoming Credit Hurdles and Historical Claims

A contractor’s personal and business credit score directly impacts their bond eligibility and premium rates. If a business owner has a rocky credit history, past legal disputes with owners, or, worst of all, a history of claims filed against previous bonds, securing favourable terms becomes an uphill battle.

How Can Contractors Overcome these Challenges?

Navigating the bonding process requires a proactive strategy. To improve their chances of approval, construction companies should focus on:

- Implementing clean, disciplined corporate financial practices and utilising CPA-prepared statements.

- Scaling project sizes incrementally rather than attempting massive, high-risk operational leaps all at once.

- Partnering with an experienced, specialized surety bond broker who understands the nuances of the construction market and can present their business to underwriters in the best possible light.

How Can Contractors Qualify for a Surety bond?

Qualifying for a construction surety bond is very similar to securing a major corporate line of credit. Because underwriters are assuming a portion of your operational risk, they evaluate applications using what the industry refers to as the Three Cs: Capital, Capacity, and Character.

To successfully clear this vetting process, contractors must systematically demonstrate their financial health, field experience, and organisational capability. Here is exactly what underwriters look for and how you can position your business to qualify:

The Critical Evaluation Factors

- Financial Strength: This is the foundation of your application. Underwriters look for a strong balance sheet with healthy working capital and reliable, positive cash flow. They will thoroughly analyse your debt-to-equity ratio and liquid assets to ensure your business can absorb sudden material price hikes or unexpected project delays without risking default.

- Operational Performance: You must prove you have the technical machinery, manpower, and management skills to execute the job. Underwriters favour contractors who have a consistent track record of delivering projects on time, within budget, and up to technical specifications. They will look closely at your past project sizes to ensure you aren’t attempting an unrealistic operational leap.

- Credit and Reputation: Your business history speaks volumes. A solid business and personal credit score, a reputation for resolving disputes promptly, and clean legal records are essential. Underwriters want to know they are backing a leadership team that operates with integrity and sound business ethics.

Actionable Steps to Improve Your Bonding Eligibility

If you want to maximise your bonding capacity and secure the most favourable premium rates, focus on these five strategic areas:

- Upgrade Your Financial Reporting: Move away from basic in-house bookkeeping. Invest in Certified Public Accountant (CPA)-prepared or audited financial statements. Clean, professional, and transparent financial records immediately build trust with underwriters.

- Build a Strategic Project Portfolio: Scale your business incrementally. Successfully complete smaller and mid-sized projects to build a verifiable resume of success before applying for bonds on massive megaprojects.

- Optimise Your Credit Profile: Actively manage your corporate debt and ensure all trade lines, supplier invoices, and credit accounts are paid on time to keep both personal and commercial credit scores pristine.

- Refine Internal Project Management: Show underwriters that you have tight control over your operations. Implement robust project tracking tools, maintain accurate Work-in-Progress (WIP) reports, and establish clear safety protocols.

- Partner with a specialised surety broker: Don’t rely on a general insurance agent. Work with a dedicated surety bond broker who specialises in the construction industry. They speak the underwriters’ language, know which surety companies fit your business profile, and can help structure your application for a higher chance of approval.

Conclusion

Surety bonds play a vital role in the construction industry by providing financial security, promoting accountability, and ensuring contractual obligations are fulfilled. As infrastructure development grows, they have become an indispensable risk management tool for both public and private sector projects.

Whether you are bidding for a new project or looking for a capital-efficient alternative to traditional bank guarantees, partnering with an experienced provider simplifies the entire process. At SafeTree, we help businesses secure tailored surety bond solutions that mitigate risk, unlock working capital, and empower you to pursue your next major growth opportunity with absolute confidence.