How to Pick the Right Surety Bond for Your Business Needs?

In today’s business environment, especially in infrastructure, construction, and government procurement, surety bonds have become essential. The issue, however, is that numerous companies seek a bond without a complete grasp of which specific type is best suited to their particular contract, the size of their project, or their financial standing.

Picking the wrong surety bond can throw a wrench in your plans, leading to approval holdups, inflated expenses, and, in the worst-case scenario, exclusion from the bidding process. This guide offers a clear and actionable approach to selecting the right surety bond for your business.

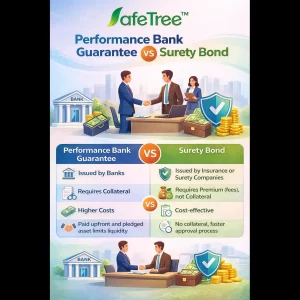

Understanding the Role of a Surety Bond

A surety bond is a three-party agreement. The principal is the business or contractor required to obtain the bond. The obligee is the project owner or authority requiring the bond. And the surety is the bond provider guaranteeing the principal’s obligations.

Unlike traditional insurance, a surety bond guarantees performance or compliance. If the principal fails to fulfil contractual obligations, the surety compensates the obligee, and the principal must reimburse the surety. Because of this financial responsibility, choosing the correct bond type is really important.

Step 1: Identify the Nature of Your Obligation

The first stage is to figure out why you need the bond. Think about it: Is this for a government contract? Is it necessary after getting a contract? Is it for following the rules? Is it related to how well the supply or service works?

You need different bonds for different duties. If you need a bid bond and apply for a performance bond instead, your application could be denied.

Step 2: Select the Correct Type of Surety Bond

The following are the most common varieties in India:

- At the bidding stage, a bid bond is given. This is a pledge to the authority that the bidder will accept the contract if they are picked and give them more proof.

- Once the contract is signed, the performance bond goes into effect. Its goal is to make sure that the contractor follows the project’s instructions.

- A payment bond makes sure that suppliers and subcontractors will get paid.

- A maintenance bond covers any problems with the work or flaws that come up within the warranty period after a project is finished.

The details of your contract will determine which bond is best for you.

Step 3: Assess Contract Value and Bond Amount

Most of the time, surety bonds are worth a certain percentage of the contract value. Bonds are often needed for government and infrastructure projects. The amount of the bond is usually between 1% and 10% of the contract’s value, depending on how risky the project is.

Before you put your name on a bond, it’s crucial to understand a few key details: the required percentage, the bond’s duration, and the procedures for extending it if needed. Choosing a bond with the wrong terms could render your submission invalid.

Step 4: Evaluate Your Financial Strength

At the heart of surety underwriting lies financial strength. Bonding companies scrutinize your net worth, creditworthiness, cash flow, the robustness of your balance sheet, and any current project obligations.

Robust financials can translate into lower premiums and a greater chance of approval. Conversely, firms with less-than-stellar financial histories might face higher costs or additional security requirements. A candid evaluation of your financial position is essential before you begin the application process.

Step 5: Review Eligibility Criteria Carefully

Each bond provider has underwriting standards. Some may focus more on project experience, while others emphasise financial metrics.

Your history of completing projects, your experience in the field, any past legal issues, your current debt load, and the general state of your business are all factors considered. Choosing a provider that aligns with your particular requirements and circumstances boosts your likelihood of approval.

Step 6: Compare Bond Providers Strategically

Not all surety providers offer the same service quality. When comparing options, consider a few important things.

Experience in Surety Products: Some insurers specialise in bonds, while others treat them as secondary offerings.

Approval Turnaround Time: In tender environments, speed matters. You don’t want to miss a deadline because of slow processing.

Relationship with Authorities: Recognised sureties may improve credibility with certain government departments.

Claim Handling Process: Understanding how disputes are handled is essential before committing.

Step 7: Understand Premium Structure

The costs of surety bonds are not the same as those of conventional insurance. They rely on how much risk you are willing to take, how much the bond is worth, how complicated the contract is, how strong your finances are, and how long the bond is.

The principle is nonetheless responsible for claims, unlike insurance. So, premium pricing is based on the risk of underwriting, not the risk of pooling.

Step 8: Examine Legal Wording and Conditions

The wording of a bond is quite important. Always read the conditions about the claim trigger, the limit of obligation, the exclusions, the extension terms, and the termination clauses.

Even tiny changes in wording can change how much liability you have. Talk to a lawyer before you make your final decision if you need to. It’s worth the extra work.

Step 9: Consider Long-Term Bonding Capacity

If your organisation bids on more than one project, don’t only consider one bond. A long-term surety partnership can help you bond more, get approvals faster, work on more than one project, and lessen your overall administrative burden. Planning for expansion makes sure that things keep going and makes bidding easier in the future.

Common Mistakes to Avoid during selection of Surety Bonds

Many businesses make avoidable errors when selecting bonds. Here’s what to watch out for:

- Applying without reading tender conditions

- Ignoring bond validity requirements

- Underestimating financial disclosure needs

- Choosing providers based only on price

- Not reviewing claim provisions

Avoiding these mistakes improves compliance and credibility.

Conclusion

Selecting the appropriate surety bond goes beyond simply fulfilling a bid requirement. It’s a matter of protecting your company’s standing, ensuring sound financial practices, and fostering enduring confidence with project owners and other involved parties. The initial step involves a thorough grasp of your contractual commitments. Next, assess your financial resources, compare different providers with care, scrutinise the legal stipulations, and ensure your choice aligns with a long-term bonding plan.

At SafeTree, we hold the view that a well-designed surety solution should accomplish more than just securing a single contract. It should facilitate sustainable growth, bolster your reputation, and position your business favourably for future prospects.

Disclaimer:

This blog is for general informational and educational purposes only. The information related to insurance is provided for general guidance only. Before selecting any insurance policy, readers are advised to consult our insurance experts for detailed advice based on their individual needs.

Published by: A2V Insurance Brokers Pvt. Ltd. (SafeTree)

Share this post:

Facebook Twitter LinkedIn WhatsApp