In the world of building and business contracts, you have to make sure you’re committed to a project. You need a financial tool that shows you can deliver, whether you’re competing on a government contract or a private infrastructure project. The performance bank guarantee has been the default choice for a long time. But as companies explore better ways to handle their cash flow, the surety bond has become a popular choice in India.

So, which one is best for your business? This guide explains the differences and helps you choose the best security solution for your next contract.

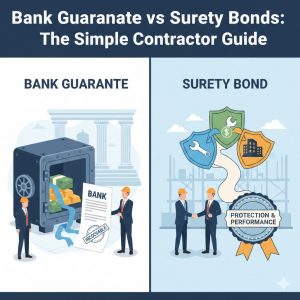

What is a performance bank guarantee?

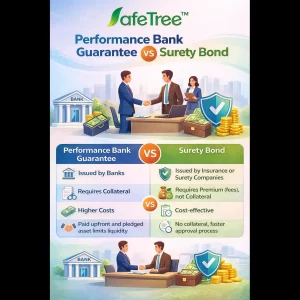

A Performance Bank Guarantee (PBG) is a promise from a bank to a contractor that they will meet their contractual commitments. It serves as a security measure in contracts, especially in fields like construction, infrastructure, and government bidding. If the contractor doesn’t finish the job or doesn’t follow the terms they committed to, the bank steps in and pays the project owner a set amount to make up for it.

A performance bank guarantee is a great way for the beneficiary to protect their money, but it usually means that contractors have to put up collateral or keep margin money with the bank. This amount will be locked up for the whole project, which might have a big effect on your working capital and available credit.

What is a surety bond?

Now let’s have a look at the modern option. A surety bond is a three-party agreement in which an insurance company promises the project owner that the contractor will do what they said they would do. A surety bond is an insurance-based product, while a bank guarantee is a financial product.

The main distinction is that the insurer doesn’t look at how much money you have in the bank. Instead, they look at your history, your financial health, and your ability to finish the project. What matters more is your proven talent than what’s in your bank account.

Key Differences between Performance Bank Guarantee vs Surety Bond

| Feature | Performance Bank Guarantee (PBG) | Surety Bond |

| Provider | Commercial Banks | Insurance Companies |

| Collateral | Usually requires 100% or high-margin money | Minimal to no collateral required |

| Liquidity | Ties up your working capital | Frees up your cash for operations |

| Bank Limits | Reduces your borrowing capacity | Does not affect your bank credit limits |

Why Surety Bonds Are the Smarter Choice for Growth?

When a business is growing, having cash on hand is quite important. A performance bank guarantee locks up your money. You can’t use the ₹1 crore you have locked up in a PBG to buy raw materials, pay workers, or pay for your next project.

You may keep your money liquid by choosing a surety bond. These bonds are backed by insurance companies, so they don’t affect your bank’s credit restrictions. This means you can bid on more than one project at a time without putting too much strain on your finances or running out of money to deal with. For contractors who want to grow, such flexibility might make the difference between staying stagnant and truly growing.

Conclusion

It depends on your project’s needs and your financial goals whether you should get a performance bank guarantee or a surety bond. Both give the project owner the protection they need, but the surety bond gives modern contractors the freedom and cash flow they need to grow.

We at SafeTree know that every contract is a chance to grow. We help organisations use these financial tools to locate the best security choices that are also the least expensive and use the least amount of resources. Today, let SafeTree help you keep your projects safe so you can build a better future.

Disclaimer:

This blog is for general informational and educational purposes only. The information related to insurance is provided for general guidance only. Before selecting any insurance policy, readers are advised to consult our insurance experts for detailed advice based on their individual needs.